LSTM versus Transformers: A Practical Comparison of Deep Learning

Models for Trading Financial Instruments

Daniel K. Ruiru

1 a

, Nicolas Jouandeau

2 b

and Dickson Odhiambo

1 c

1

Starthmore University, Nairobi, Kenya

2

Universit

´

e Paris 8, Saint-Denis, France

{druiru, dowuor}@strathmore.edu, n@ai.univ-paris8.fr

Keywords:

Deep Learning, Recurrent Neural Networks, Long Short Term Memory (LSTM), Transformers.

Abstract:

Predicting stock prices is a difficult but important task of the financial market. Often two main methods

are used to predict these prices; fundamental and technical analysis. These methods are not without their

limitations which has led to the use of machine learning by analysts and investors as they try to gain an edge

in the market. In this paper, a comparison is made between recurrent neural networks and the Transformer

model in predicting five financial instruments; Gold, EURUSD, GBPUSD, S&P500 Index and CF Industries.

This comparison starts with base models of LSTM, Bidirectional LSTM and Transformers. From the initial

experiments, LSTM and Bidirectional LSTM have consistent results but with more trainable parameters. The

Transformer model then has few trainable parameters but has inconsistent results. To try and gain an edge from

their respective advantages, these models are combined. LSTM and Bidirectional LSTM are thus combined

with the Transformer model in different variations and then trained on the same financial instruments. The

best models are then trained on the larger datasets of the S&P500 index and CF Industries (1990-2024) and

their results are used to make a simple trading agent whose profit and loss margin (P/L) is compared to the

2024 Q1 returns of the S&P500 index.

1 INTRODUCTION

Predicting stock prices is a difficult task owing to the

ever changing and unpredictable nature of the finan-

cial market. Today, this goal of forecasting financial

markets has garnered a lot of attention from both aca-

demic and industrial practitioners who hope to pro-

vide provable answers for price outcomes. Many

methodologies have been suggested, often falling

within two major categories; technical and fundamen-

tal analysis (Kehinde et al., 2023). The former de-

fines techniques that evaluate investments based on

price patterns/trends while the latter focuses on the

intrinsic value of assets as well as the factors that

influence price outcomes (Krishnapriya and James,

2023). While somewhat effective, these methods still

face serious difficulties in providing solid answers or

even forecast of financial prices as exemplified by sig-

nificant fluctuations such as the 2008 financial crisis

which unfolded despite the existing technical and fun-

a

https://orcid.org/0000-0003-3197-8821

b

https://orcid.org/0000-0001-6902-4324

c

https://orcid.org/0000-0002-0968-5742

damental analyses. As such, a new phenomenon of

using machine learning algorithms to predict finan-

cial markets has been gaining popularity owing to the

success of these techniques in other domains. Ma-

chine learning methods use data to provide predic-

tions which academics and market traders/regulators

can use to forecast prices. Frameworks like Long

Short Term Memory Neural Networks (LSTMs) and

other Recurrent Neural Networks (RNNs) are of par-

ticular interest in the financial domains because of the

demonstrated superiority in dealing with time series

problems (Fischer and Krauss, 2018a). LSTM further

stands out as it has the ability to exploit and retain se-

quential data patterns over long periods of time. Re-

cently, this attribute of LSTM was enhanced through

the use of Transformers which shine in handling long

dependencies of input elements on top of enabling

parallel processing (Vaswani et al., 2017). Trans-

formers have thus become more effective in deal-

ing with tasks that use sequential data which explain

their popularity in Natural Language Processing do-

main. A similar challenge is exhibited by the finan-

cial markets as they pose a task in the sequential deci-

sion making problem domain which this paper tries to

Ruiru, D., Jouandeau, N. and Odhiambo, D.

LSTM versus Transformers: A Practical Comparison of Deep Learning Models for Trading Financial Instruments.

DOI: 10.5220/0012981100003837

Paper published under CC license (CC BY-NC-ND 4.0)

In Proceedings of the 16th Inter national Joint Conference on Computational Intelligence (IJCCI 2024), pages 543-549

ISBN: 978-989-758-721-4; ISSN: 2184-3236

Proceedings Copyright © 2024 by SCITEPRESS – Science and Technology Publications, Lda.

543

solve. This paper compares LSTM and Transformers

through their performance in predicting a variety of fi-

nancial instruments. Moreover, these two algorithms

are combined to try and yield a superior prediction

model.

The rest of the paper is organized as follows. Sec-

tion 2 outlines the Related Works, Section 3 briefly

discusses the Methodology, section 4 then reviews the

Experiments which is then followed by the Results

and Discussions in Section 5. Finally, Section 6 con-

cludes the study.

2 RELATED WORKS

Deep learning algorithms have shown great model-

ing prowess with non-linearity problems. LSTM and

Transformers can learn a lot of information from se-

quential data which explains their recent application

in complex time series modeling problems such as

stock/financial price prediction (Lin, 2023). The ap-

plication of these algorithms in the financial domain

are discussed below.

2.1 LSTM and Bidirectional LSTM

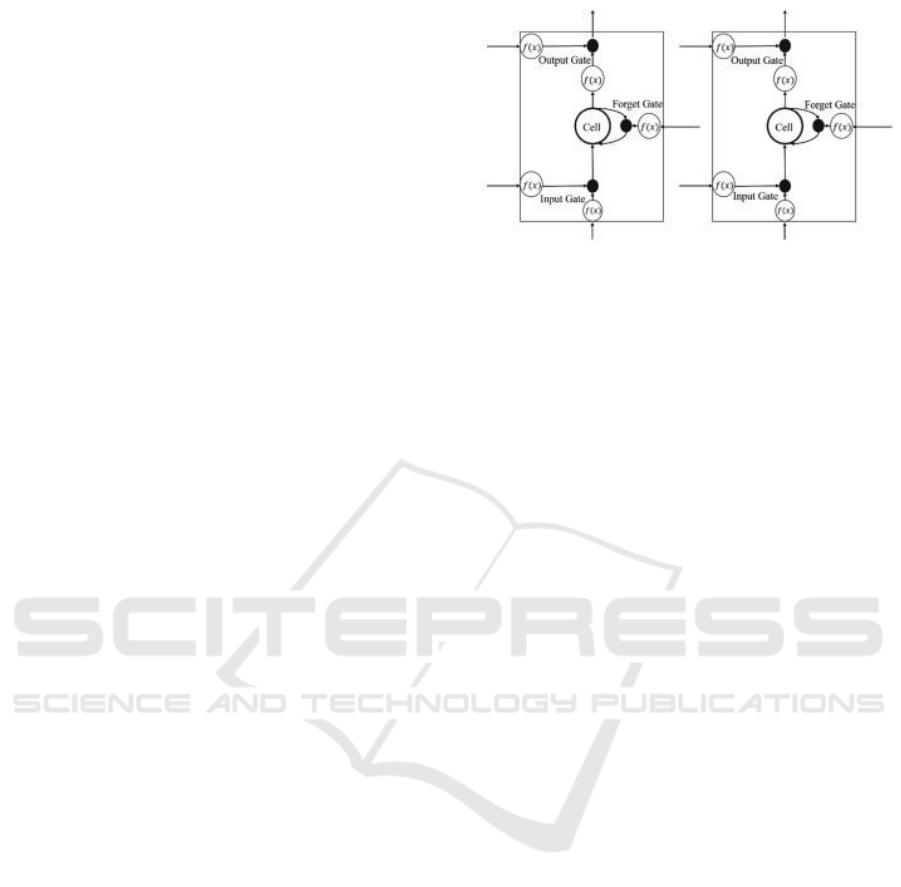

The LSTM model is actually a type of recurrent neu-

ral network (RNN) that was developed for modeling

sequential data. It uses gate units to manage the flow

of information which addresses the issues of gradi-

ent vanishing and explosion found in conventional

RNNs (Hochreiter and Schmidhuber, 1997). The ba-

sic LSTM structure shown in Figure 1 outlines a base

architecture that includes input gates, forget gates

and output gates. These gates selectively discard or

allow information flow through the network which

helps LSTM handle long sequences of information

and have better memory effect for any recurring pat-

terns. The input, forget and output gates are described

the following equations:

i

t

= σ(ω

i

[h

t−1

,x

t

] + b

i

) (1)

f

t

= σ(ω

f

[h

t−1

,x

t

] + b

f

) (2)

o

t

= σ(ω

o

[h

t−1

,x

t

] + b

o

) (3)

Where: i

t

is the input gate, f

t

is the forget gate, o

t

is

the output gate, σ is the sigmoid function, w

x

are the

weights of the respective gates, h

t−1

are the outputs

of the previous lstm block, x

t

is the input of the cur-

rent timestamp and b

x

are the biases for the respective

gates.

The mentioned attribute of LSTM make it ideal

for financial price modeling as it facilitates the ex-

ploration of long term dependencies found in mar-

ket prices. Many scholars and industrial practition-

Figure 1: Basic LSTM Structure.

ers have applied this basic structure in the financial

market. (Roondiwala et al., 2017); (Cao et al., 2019);

(Bao et al., 2017); (Fischer and Krauss, 2018b) all

used LSTM as a deep learning model for predicting

the financial market. In some cases, like that of (Bao

et al., 2017) they combined this base LSTM structure

with stacked auto encoders which yielded better re-

sults. In other cases, like that of (Siami-Namini et al.,

2019), bidirectional LSTM (BiLSTM) have been used

to increase the prediction performance by learning

long term dependencies across time steps of sequence

of data (time series) in both directions. This varia-

tion of LSTM is useful if a problem requires an RNN

to acquire information about an entire time series at

various iterations.

2.2 Transformers

On its part, Transformers are deep learning models

that also handle sequential data but unlike RNNs they

use a self-attention mechanism across their encoder-

decoder pair. At a high level, transformers can even

be seen as a sequence to sequence model but with an

encoder-decoder pair. The encoder is used to encode

the input sequence while the decoder produces the

output sequence (Vaswani et al., 2017); (Lin, 2023).

The self-attention mechanism found in this structure

then help to effectively pass information between the

encoder-decoder pair in both directions. Moreover,

self-attention also increases the encoding of the in-

put sequence by the encoder. Figure 2 illustrates a

simple transformer architecture. The said attention

mechanism is facilitated by three vectors from the en-

coder’s input vectors. These three vectors are known

as Query (Q), Key (K) and Value (V) which are sim-

ply abstractions used to calculate transformers atten-

tion. In summary, these vectors are combined with a

softmax function to give the attention mechanism as

shown in equation 4. The role of the softmax func-

tion is to convert raw attention scores into probability

distributions.

NCTA 2024 - 16th International Conference on Neural Computation Theory and Applications

544

Figure 2: A Simple Transformer Architecture.

Attention(Q,K,V ) = so f tmax(QK

T

/

p

d

k

)V (4)

Today, Transformers have shown great efficiency

and versatility which have led to their extensive use

in many sequential decision making tasks. In partic-

ular, their ability to handle long sequence of data and

parallel process all the available data makes them su-

perior in capturing long range dependencies like those

in NLP and long term financial results/assessments.

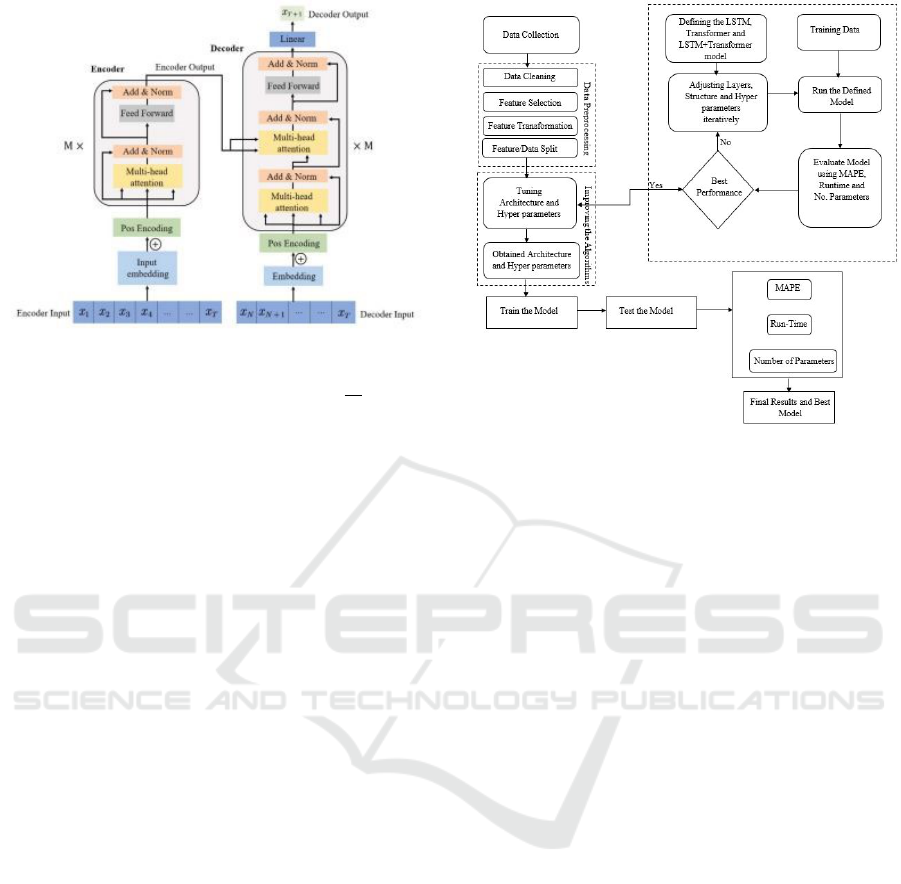

3 METHODOLOGY

3.1 Defining the Problem

This paper uses LSTM and Transformers together

with their variants as reviewed in the literature re-

view. There was also an initial focus on the broadest

samples of these deep learning models, with modifi-

cations made to both the architecture and parameters.

The predictions made were done in four stages. First,

data collection, where a variety of datasets were ob-

tained to evaluate the proposed models’ performance.

Second, data pre-processing where the collected data

was enhanced to meet the requirements of the defined

models. Third, LSTM, Transformer and LSTM +

Transformer architecture and parameter optimization

to achieve the best results possible. Finally, predic-

tions were made based on trade simulations. Figure 3

summarizes this general road-map used in the experi-

ments of this paper.

3.2 LSTM and Transformer

To develop the final models used to predict financial

instruments, defining the problem also involved mod-

ifying the two base models LSTM and Transformer.

Figure 3: The General Road-Map.

To start with, a conventional unidirectional LSTM

and Bidirectional LSTM were used. These base mod-

els were then trained on the financial instruments with

their results recorded based on the evaluation met-

rics identified below (MAPE, Run-time and number

of parameters). Thereafter a basic transformer model

was implemented. This transformer model was then

trained on the financial instruments identified for this

study and the results were recorded based on the eval-

uation metrics.

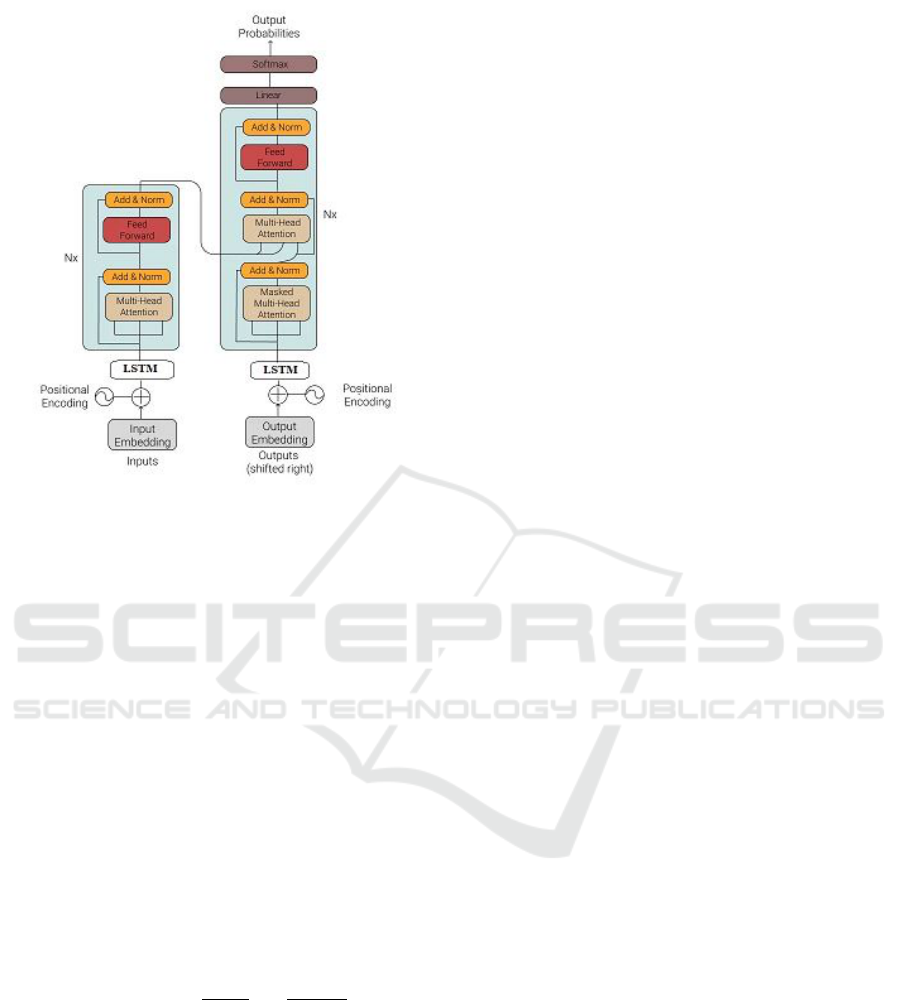

3.3 Combining LSTM and

Transformers

Finally, the (best performing) LSTM model (based

on variation of layers) and Transformer model were

combined. In this case, the LSTM layer was added

just before the attention block of the Transformer as

illustrated in Figure 4. This resultant LSTM + Trans-

former model was then trained on the financial in-

struments and the results were recorded based on the

same evaluation metrics used in the previous models

training. This combination was the final step of the

experiments conducted.

3.3.1 Combining BiLSTM and Transformers

To cover the baseline model, Bidirectional LSTM was

also introduced. A similar structure was followed

with the combination of Bidirectional LSTM with

Transformer where the BiLSTM layer(s) was placed

before the attention block of the Transformer model.

LSTM versus Transformers: A Practical Comparison of Deep Learning Models for Trading Financial Instruments

545

Figure 4: Combining LSTM and Transformer.

3.4 Evaluation Metrics

Many evaluation metrics exist to assess the accuracy

of predicted results each with their own benefits. For

the experiments conducted, one conventional metrics

was used Means Absolute Percentage Error (MAPE)

owing to its ability to define the accuracy of forecast-

ing methods. MAPE outlines the average of the ab-

solute percentage errors of each entrant in a dataset

which then calculates how accurate a forecasted re-

sult is compared to an actual result (Jierula et al.,

2021). The choice of MAPE was also driven by its

ability to effectively analyze large sets of data such

as those found with the datasets used in this paper’s

experiments. Reviewing MAPE is also a straightfor-

ward process, with a 10 percent MAPE indicating a

10 percent deviation between the predicted value and

the actual value. Equation 5 summarizes MAPE.

MAPE(y, ˆy) =

100%

N

N−1

∑

i=0

|y

i

− ˆy

i

|

|y

i

|

(5)

In addition to MAPE, Run Time and Number of

Parameters used per model were used to assess the fi-

nal results. Generally, the prediction accuracy of any

model was not solely judged by the deviation from

the true value but also on the time it took to achieve

its predicted values (Run Time). Also, the number

of parameters used was a factor as they define the

resources used to run any given model. As such, in

an ideal case, a high accuracy of the predicted results

would be achieved with minimal run time and min-

imum number of parameters. As such, while trying

to achieve high performance/accuracy, the developed

model was expected to have minimal training param-

eters and run-time.

4 EXPERIMENTS

This section highlights two things; the datasets used

and the experiments done. The evaluations summa-

rized by this paper were based on five financial in-

struments - three forex pairs (Gold, GBPUSD, and

EURUSD); S&P500 (a stock market index) and CF

Industries Holdings stock prices (one of the stocks in

S&P500 index).

4.1 Data Selection and Preprocessing

The experiments done were based on large dataset for

all the five instruments. For the first 2 experiments

data from the 1st January 2013 to 2024 was used.

From experiment 3 to 5, only S&P500 and CF data

was used. The data used here was also larger, as it in-

cluded the period 1990 to 2024. In all the dataset, the

data collected was of the OHLC format (Open-High-

Low-Close). To get more stable analysis and results,

the daily time frame was used. The data was collected

from Yahoo Finance using the “yfinance” API. The

S&P500 and CF dataset was also manually obtained

from Stooq (stooq.com), an online resource that pro-

vides historical data for indices, stocks, bonds, forex

and other form of financial data.

4.2 Experiment 1

To get a benchmark for the experiments, the three

main models; LSTM, Bidirectional LSTM and Trans-

former were trained on the five financial instruments.

For the LSTM model, a base architecture with one

layer of 128 units was used, ultimately generating

73265 trainable parameters. A similar number of lay-

ers and units was used for the Bidirectional LSTM

(i.e. 1 layer with 128 units) and the total number

of trainable parameters ended being 146225. Finally,

the transformer model was based on a single trans-

former block which was then replicated to have the

needed number of blocks. For a start, 4 transformer

blocks were used resulting in 17205 trainable param-

eters. These three models were used to conduct the

first round of experiments with rankings being done

based on MAPE, Run-time and the number of param-

eters used to achieve their results. The results of this

first round (Experiment 1) are highlighted in the Re-

sults and Discussion section.

NCTA 2024 - 16th International Conference on Neural Computation Theory and Applications

546

4.3 Experiment 2

In an attempt to combine LSTM and Transformer to

yield a superior model, several variations of LSTM +

Transformers were developed and trained on the five

financial instruments. First, there was the base LSTM

with 1 layer of 128 units plus the basic four block

transformer model (here named LSTM128+TX).

Subsequently, LSTM with one layer of 64 units, 32

units and three layers of 128, 64 and 32 units were

combined with the transformer model (there naming

following a similar pattern as LSTM128+TX). Sim-

ilarly, the Bidirectional LSTM was combined with

the transformer model with a familiar naming pattern:

BiLSTM128+TX, BiLSTM64+TX, BiLSTM32+TX

and BiLSTMAll+TX. These combinations and the

number of trainable parameters used are summarized

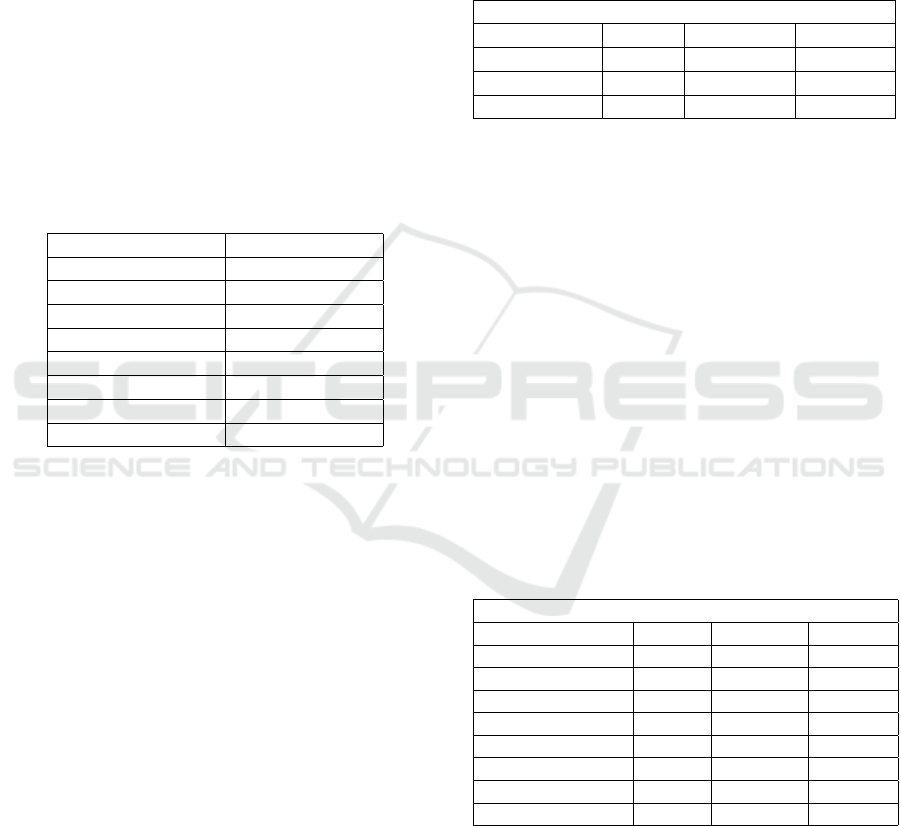

below in Table 1.

Table 1: Combined Models and Number of Parameters.

Model No. Parameters

LSTMAll + TX 833394

LSTM128 + TX 1523346

LSTM64 + TX 651474

LSTM32 + TX 301554

BiLSTMAll + TX 2083794

BiLSTM128 + TX 3430930

BiLSTM64 + TX 1392274

BiLSTM32 + TX 618706

These combinations of LSTM/BiLSTM and

Transformer were then ranked based on their MAPE,

Run-time and number of parameters. The results of

these tests (Experiment 2) are highlighted in the Re-

sults and Discussion section.

4.4 Experiment 3

For the third experiment, the three best models, (ei-

ther base model or combination models) were then

used to predict the S&P500 index and CF industries.

Prior to experiment 3, a quick summary of the best

performing models, based on experiment 1 and 2 was

done to help identify the 3 best models.

4.5 Experiment 4 and 5

In this final round of experiments, the two financial

instruments (S&P500 and CF Industries) were pre-

dicted with the three best models from experiment

3. Also, this final round of experiment saw an in-

depth review of the prediction of the CF industries

prediction by the best model. Thereafter, this pre-

diction/forecast was compared with the returns of in-

vesting in the S&P500 index in the last month of the

dataset used. In all, this final test was to see whether

the best model from these experiments would chal-

lenge the returns of the S&P500 index in 2024.

5 RESULTS AND DISCUSSIONS

Table 2: Sample of Experiment 1 Results - Gold.

Experiment 1: Gold

Model MAPE Run-Time No. Para

LSTM128 0.0143 84.27s 73265

BiLSTM128 0.0134 51.50s 146225

TX 0.0134 150.24s 17205

The Tables 2 and 3 highlight a sample of the results of

the first and second experiment where all models were

tested with the five financial instruments. From ex-

periment 1, one results that stood out was the lack of

consistency in the results of the Transformer model.

Over a run of multiple training iterations including

some of the same parameters and financial instru-

ments, the Transformer model failed to have similar

or comparable results. Moreover, the first experiment

also broke a notion that was held at the start of the

tests that the fewer number of parameters in the Trans-

former model would results in a shorter run-time. Sur-

prisingly, the Transformer model regularly took the

longest time to run the training but yielded compet-

itive results. On their part, the LSTM and Bidirec-

tional LSTM were more consistent with their results,

including have comparable outcomes in multiple iter-

ations of same financial instruments.

Table 3: Sample of Experiment 2 Results - Gold.

Experiment 2: Gold

Model MAPE Run-Tim No.Para

LSTMAll+TX 0.0140 351.37s 833394

LSTM128+TX 0.0155 333.65s 1523346

LSTM64+TX 0.0183 213.63s 651474

LSTM32+TX 0.0168 151.58s 301554

BiLSTMAll+TX 0.0147 604.48s 2083794

BiLSTM128+TX 0.0142 518.57s 3430930

BiLSTM64+TX 0.0199 280.53s 1392274

BiLSTM32+TX 0.0186 221.33s 618706

On experiment 2, the combination of

LSTM/BiLSTM with Transformer model pro-

duced models that had consistent results. It was

much easier to replicate a prediction with them which

validated their use. Of note was the Run-time of the

BiLSTMAll+TX and BiLSTM128+TX which was

often the longest in any of the categories tested. This

outcome is easily attributed to the total number of

LSTM versus Transformers: A Practical Comparison of Deep Learning Models for Trading Financial Instruments

547

trainable parameters used; 2083794 and 3430930

respectively.

Figure 5: Sample Experiment 2 - LSTMAll+TX.

The ranking done in experiment three saw, 3 mod-

els emerge as favorite based on their leading perfor-

mance in MAPE, Run-time and number of training

parameters (fewer being better). The three models

were LSTM with 1 layer of 32 units combined with

Transformer (LSTM32 + TX), the base Transformer

model (TX) and the base Bidirectional LSTM (with

1 layer of 128 units). These three were then used in

experiment 4 and 5 where tables 4 and 5 summarizes

the overall results.

Table 4: Sample of Experiment 4 Results - S&P500 Index.

Experiment 4: S&P500 Index

Under 75 epochs

Model MAPE Run-Tim No.Para

LSTM32+TX 0.0149 949.04955s 301554

TX 0.0207 553.503s 17205

Bi-LSTM 0.01509 350.8049s 146225

Under 300 epcohs

LSTM32+Tx 0.01964 986.7037s 301554

TX 0.02699 547.1845s 17205

Bi-LSTM 0.01334 543.042s 146225

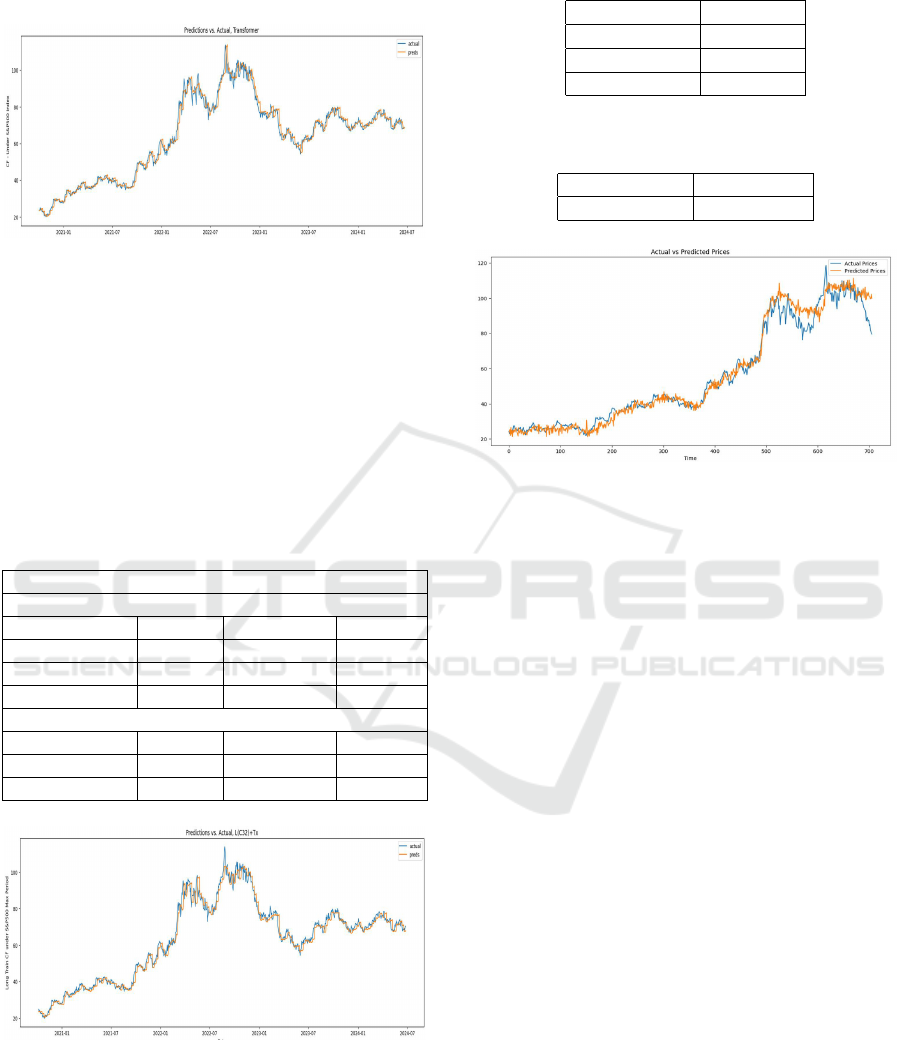

Figure 6: Experiment 4 - Prediction of CF Industries.

From these results it is clear that the combined

model of LSTM and Transformer outperforms all the

other models in predicting CF Industries. This obser-

vation further led to the development of a basic trad-

ing agent that used the LSTM32+TX model. While

its performance changed rapidly, the best, positive re-

Table 5: Experiment 5 - Predicting CF Industries.

Model Accuracy

LSTM32+Tx 95.9154%

TX 93.2079%

Bi-LSTM 91.6369%

Table 6: Experiment 5 - Trading CF Industries with

LSTM32+TX Based Agent.

Model-Agent %Change

LSTM32+Tx 0.012-0.768

Figure 7: Visualizing CF Industries Trading.

sults (profitable P/L) ranged between 1.2 percent to

7.68 percent return on initial investment which is not

bad compared to the S&P500 index 2024(Q1) returns

of about 15 percent (Curvo, 2024); (Speights, 2024).

Therefore, with good risk management, a potential

trader could get good returns by combining funda-

mental and technical analysis with an LSTM + Trans-

former model.

6 CONCLUSIONS

In this paper, LSTM, Bidirectional LSTM and Trans-

former models were compared in predicting five fi-

nancial instruments. From an initial forecast, three

best performing models were used to further pre-

dict S&P500 index and CF Industries based on large

datasets. The best model was then tested as a trading

agent model which yielded good results. This agent

however had erratic results which is solid ground for

future works, as one tries to stabilise the trading out-

comes. In future works, one can try to stabilize the

trading results by either adding more trading heuris-

tic, modifying the base model or changing the speci-

fication of the trading environment.

NCTA 2024 - 16th International Conference on Neural Computation Theory and Applications

548

REFERENCES

Bao, W., Yue, J., and Rao, Y. (2017). A deep learning

framework for financial time series using stacked au-

toencoders and long-short term memory. PloS one,

12(7):e0180944.

Cao, J., Li, Z., and Li, J. (2019). Financial time series fore-

casting model based on ceemdan and lstm. Physica A:

Statistical mechanics and its applications, 519:127–

139.

Curvo (2024). S&P 500: historical performance from 1992

to 2024. [Online; accessed 9. Jul. 2024].

Fischer, T. and Krauss, C. (2018a). Deep learning with long

short-term memory networks for financial market pre-

dictions. European journal of operational research,

270(2):654–669.

Fischer, T. and Krauss, C. (2018b). Deep learning with long

short-term memory networks for financial market pre-

dictions. Eur. J. Oper. Res., 270(2):654–669.

Hochreiter, S. and Schmidhuber, J. (1997). Long short-term

memory. Neural computation, 9(8):1735–1780.

Jierula, A., Wang, S., Oh, T.-M., and Wang, P. (2021). Study

on accuracy metrics for evaluating the predictions of

damage locations in deep piles using artificial neural

networks with acoustic emission data. Applied Sci-

ences, 11(5):2314.

Kehinde, T., Chan, F. T., and Chung, S. H. (2023). Scien-

tometric review and analysis of recent approaches to

stock market forecasting: Two decades survey. Expert

Systems with Applications, 213:119299.

Krishnapriya, C. and James, A. (2023). A survey on stock

market prediction techniques. In 2023 International

Conference on Power, Instrumentation, Control and

Computing (PICC), pages 1–6. IEEE.

Lin, Z. (2023). Comparative study of lstm and transformer

for a-share stock price prediction. In 2023 2nd Inter-

national Conference on Artificial Intelligence, Inter-

net and Digital Economy (ICAID 2023), pages 72–82.

Atlantis Press.

Roondiwala, M., Patel, H., Varma, S., et al. (2017). Predict-

ing stock prices using lstm. International Journal of

Science and Research (IJSR), 6(4):1754–1756.

Siami-Namini, S., Tavakoli, N., and Namin, A. S. (2019).

A comparative analysis of forecasting financial time

series using arima, lstm, and bilstm. arXiv preprint

arXiv:1911.09512.

Speights, K. (2024). The S&P 500 Jumped Nearly 15% in

the First Half of 2024. Here’s What History Says It

Could Do in the Second Half of the Year. [Online;

accessed 9. Jul. 2024].

Vaswani, A., Shazeer, N., Parmar, N., Uszkoreit, J., Jones,

L., Gomez, A. N., Kaiser, Ł., and Polosukhin, I.

(2017). Attention is all you need. Advances in neural

information processing systems, 30.

LSTM versus Transformers: A Practical Comparison of Deep Learning Models for Trading Financial Instruments

549