Improving Machine Learning Performance in Credit Scoring by

Data Analysis and Data Pre-Processing

Bogdan Ichim

1,2

and Bilal Issa

1

1

Faculty of Mathematics and Computer Science, University of Bucharest, Str. Academiei 14, Bucharest, Romania

2

Simion Stoilow Institute of Mathematics of the Romanian Academy, Str. Calea Grivitei 21, Bucharest, Romania

Keywords: Data Science, Data Analysis, Data Pre-Processing, Balanced Random Forest, Extreme Gradient Boosting,

Light Gradient Boosting Machine, Neural Networks.

Abstract: In this paper we showcase several data analysis and data pre-processing techniques which, when applied to

the dataset Give Me Some Credit, lead to improvements in the performance of several machine learning

algorithms in classifying defaulters and non-defaulters in comparison with other existing solutions from the

literature. Our study underscores the importance of these techniques in data science in general, and in

enhancing the machine learning outcomes in particular.

1 INTRODUCTION

Credit scoring is the process of evaluating

individuals’ credit worthiness based on their

financial history and behaviour (including income,

age, debt, etc.) and predicting whether they will

experience financial distress in the future. It plays a

crucial role in preventing financial losses by

avoiding loans to high-risk individuals and ensuring

that creditworthy individuals are not overlooked.

However, predicting financial distress can be

difficult, requiring a lot of data to capture underlying

patterns of defaulters and non-defaulters. In this

paper we expand on the work of (Lessmann et al.,

2015) and (Gunnarsson et al., 2021). We attempt to

address the difficulties associated with a certain

dataset from an analytical point of view and study

methods that can overcome the obstacles like

missing data, data errors and severe class imbalance.

In many papers like (Lessmann et al., 2015) and

(Gunnarsson et al., 2021) the authors assessed

various machine learning algorithms across different

datasets, without directly manipulating the data, as

their focus is on the algorithms themselves.

Consequently, we selected one dataset of moderate

complexity – which, while it doesn't achieve the

highest performance scores, it presents enough

challenges for further exploration and improvement.

The contributions made by this paper are the

following:

We have analysed the Give Me Some Credit

(GMC) dataset. This is useful for further data

pre-processing and choosing the right

techniques to apply.

Pre-processed the data to a form suitable as

input for several machine learning algorithms

(including neural networks).

We have studied the effect of imputation

algorithms on GMC dataset and their impact

on the algorithm’s performance.

Engineered seven new features that are ranked

in the top 10 most significant predictors for all

algorithms tested.

Tested a wide range of data-level class

balancing methods and compared their

performance to algorithm-level approaches,

finding the latter to be the best balancing

practice for the particular case of the GMC

dataset.

Implemented the balanced sampling strategy

found in the Balanced Random Forest

algorithm and compared its results to other

algorithms well-known for their performance

like Extreme Gradient Boosting.

Improved the state-of-the-art results by 1% in

the AUC score through our comprehensive

analysis and carefully engineered features.

The code and the pre-processed dataset used for

these experiments are available on demand.

Ichim, B. and Issa, B.

Improving Machine Learning Performance in Credit Scoring by Data Analysis and Data Pre-Processing.

DOI: 10.5220/0013118500003890

In Proceedings of the 17th International Conference on Agents and Artificial Intelligence (ICAART 2025) - Volume 3, pages 249-255

ISBN: 978-989-758-737-5; ISSN: 2184-433X

Copyright © 2025 by Paper published under CC license (CC BY-NC-ND 4.0)

249

2 RELATED WORK

In recent years machine learning has captured the

attention of academia, business and industry due to

its remarkable capacity to process vast volumes of

data in order to identify complex patterns.

In particular it allows banks and other similar

financial institutions to evaluate the credit

worthiness of companies or individuals with greater

accuracy, objectively and without bias, in order to

approve or deny loan requests.

The Give Me Some Credit dataset was first

introduced in a Kaggle competition and further was

utilized as a standard dataset for credit scoring in a

number of academic publications. Some of these

studies achieved their best results using ensemble

methods, as demonstrated by (Lessmann et al.,

2013) and (Lessmann et al., 2015), while others by

employing gradient boosting algorithms, such as in

(Gunnarsson et al., 2021) and (Gidlow, 2022).

However, most of these studies overlooked the

essential data pre-processing steps, including the

detection of outliers, data imputation, feature

engineering and class balancing, which may lead to

a suboptimal performance of the algorithms tested.

A machine learning model which proved to be

very useful in our experiments is the Balanced

Random Forest (BRF) algorithm, which is a

variation of the Random Forest (RF) algorithm. The

former algorithm makes sure that all classes in the

dataset are represented equally at the training step,

by randomly selecting the same number of samples

from all classes. This variation of the RF algorithm

makes it an ideally suited algorithm for tackling

severely unbalanced datasets, in particular for the

Give Me Some Credit dataset which will be further

analysed. For more information we point the reader

to (Chen et al., 2004).

In parallel a new architecture of neural networks

known as Attentive Interpretable Tabular Learning

(TabNet) was proposed in (Arik and Pfister, 2021).

It was developed specifically to handle tabular data,

making it a suitable neural network to be used for

handling credit data. It utilizes an attention

mechanism in order to select the most relevant

features at each decision-making stage. This allows

the model to concentrate on different subsets of

features, enhancing interpretability and functionality

on structured data.

In this paper we investigate the performance of

the BRF, TabNet and other algorithms in

combination of several data pre-processing

techniques, improving the existing solutions

proposed by other authors for the GMC dataset.

3 METHODOLOGY

3.1 Objectives and Workflow

The goal of this paper is to study the capacity of

several machine learning algorithms to assess the

credit worthiness of individuals by predicting

whether or not a default will happen in the following

two years. By conducting a deep analysis of the

problem, we also aim to improve some standard

metrics for performance which were previously

achieved by other authors. A particular aspect of the

GMC dataset is that it contains imbalanced samples

of defaulters and non-defaulters. The problem of

identifying defaulters prevails over the problem of

identifying non-defaulters in the world of credit

scoring because it helps reducing losses for the

financial institutions. As a result, the model's ability

to predict each class independently should be

considered, rather than just its accuracy.

To accomplish these objectives, we use in our

article a structured workflow. First, the structure and

the content of the GMC dataset are analysed and

understood. Next, basic data cleaning is performed,

including the removal of duplicates and the removal

of some attributes that are not relevant. After that, a

comprehensive stage of exploratory data analysis is

made in order to find potential outliers and

correlations in the data. Subsequently, a process of

feature engineering is done with the scope of adding

new features to the dataset in order to accentuate the

significance of certain features. (This turned out

later to be a crucial step for getting the best possible

outcomes.) Several class balancing methods were

also employed for addressing the severe imbalance

of the dataset, before finally applying the machine

learning algorithms.

3.2 Dataset

The Give Me Some Credit dataset was released for a

Kaggle competition which took place from

September to December 2011. It is frequently used

by various researchers in order to predict borrower

distress within two years. The dataset comprises

250,000 anonymized entries with twelve key

features, including Age, Monthly Income and Debt

Ratio. The primary target variable in these studies

(“SeriousDlqin2yrs”) indicates whether borrowers

experienced financial distress, defined as being 90

days or more overdue on any credit account within

two years (1 for distress, 0 otherwise). The GMC

dataset is considered difficult for the fact that it

contains a few features, predicts default two years in

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

250

the future and has a severe class imbalance (6.7%

defaulters) compared to other available datasets that

predict default only six months in the future and

contain more balanced samples, for example 20%

and 50% default rate in the HMEQ and the

Australian Credit respectively. The difference in the

classification performance as measured by AUC in

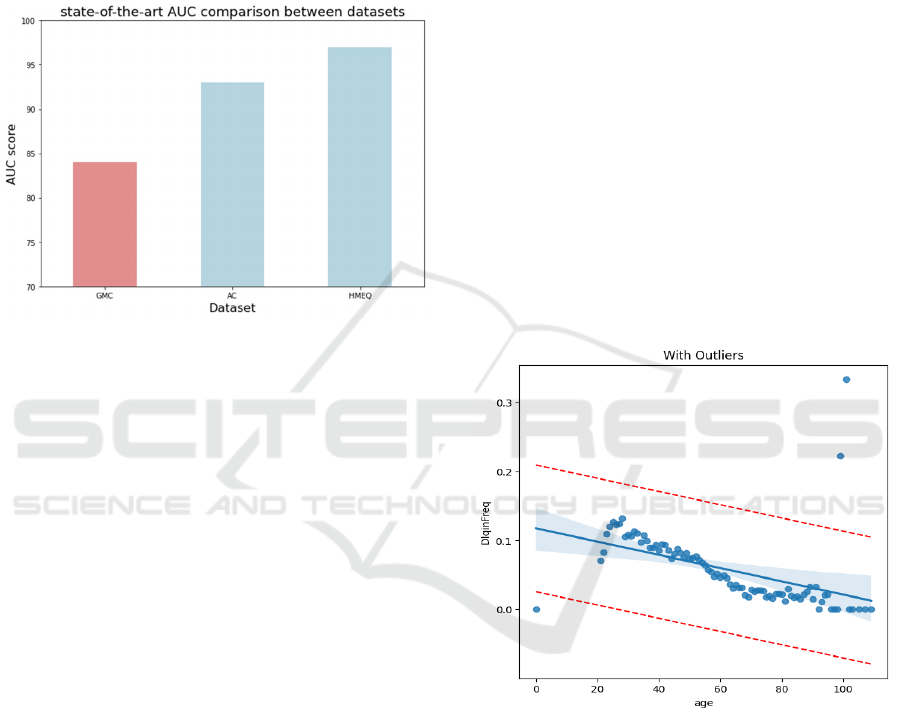

previous studies is illustrated in Figure 1.

Figure 1: Comparison between the best AUC scores

obtained on the GMC dataset in red, and the Australian

Credit (AC) and HMEQ.

3.3 Technical Implementation

To implement the code for our experiments, we have

used the programming language Python together

with libraries like TensorFlow, PyTorch and Scikit-

Learn. TensorFlow is a library developed by Google

(Google Brain, 2016) for employing neural networks

and machine learning algorithms. Another important

library is PyTorch (Paszke et al., 2019), developed

by Meta and having a similar purpose as

TensorFlow. Lastly, the most used library in our

paper is Scikit-learn (Pedregosa et al., 2011), which

contains implementations of the most popular

machine learning algorithms and can be used to

define and train various models. It also contains

other algorithms related to data pre-processing such

as imputation, data-level balancing and data splitting

algorithms.

4 DATA PRE-PROCESSING

4.1 Outlier Elimination

The first step in data pre-processing was to detect

and eliminate outliers. We tested various methods

and discovered that the Z-score and the regression

analysis proved to be the most effective techniques

among them.

The Z-score procedure automatizes the process

of detecting outliers. All data points with distance

from the mean bigger than a set number of standard

deviations are considered to be outliers. For our

project we have chosen to set the threshold at 3 after

analysing different outcomes and establishing this

threshold as being the best. For example, this

threshold correctly classified individuals whom age

is less than 18 as outliers, which is the case since the

minimum age accepted to apply for a loan is 18. In

the end 5047 entries were identifies as outliers by

this method, out of which 517 were in the defaulters

class.

The other technique which we employed in order

to eliminate outliers is the regression analysis. This

method is used to examine the relationship between

a particular predictor and a fixed target by training a

linear model and then plotting the fitted line. The

points situated beyond a certain distance from the

fitted line (measured in standard deviations) are

further identified as outliers.

Figure 2: The fitted line of the age groups and their

delinquency rate. The red lines represent the chosen

distances from the fitted line.

4.2 Imputation

In order to deal with missing values in “Monthly

Income” and “Number of dependents” columns

three methods for imputation were tested. The first

two methods were the KNN Imputer and the Simple

Imputer, chosen for their efficiency. However, the

resulting distributions and performance scores

indicate that these techniques are not suitable for the

GMC dataset. The last method was the Iterative

Improving Machine Learning Performance in Credit Scoring by Data Analysis and Data Pre-Processing

251

Imputer, which has a built-in machine learning

algorithm that sees a feature with missing values as a

target and the remaining variables as predictors in

order to iteratively input the missing values.

All three imputation outcomes were tested on

several different machine learning algorithms

(including Random Forest and Extreme Gradient

Boosting). In the end the Iterative Imputer delivered

the most satisfactory results.

4.3 Feature Engineering

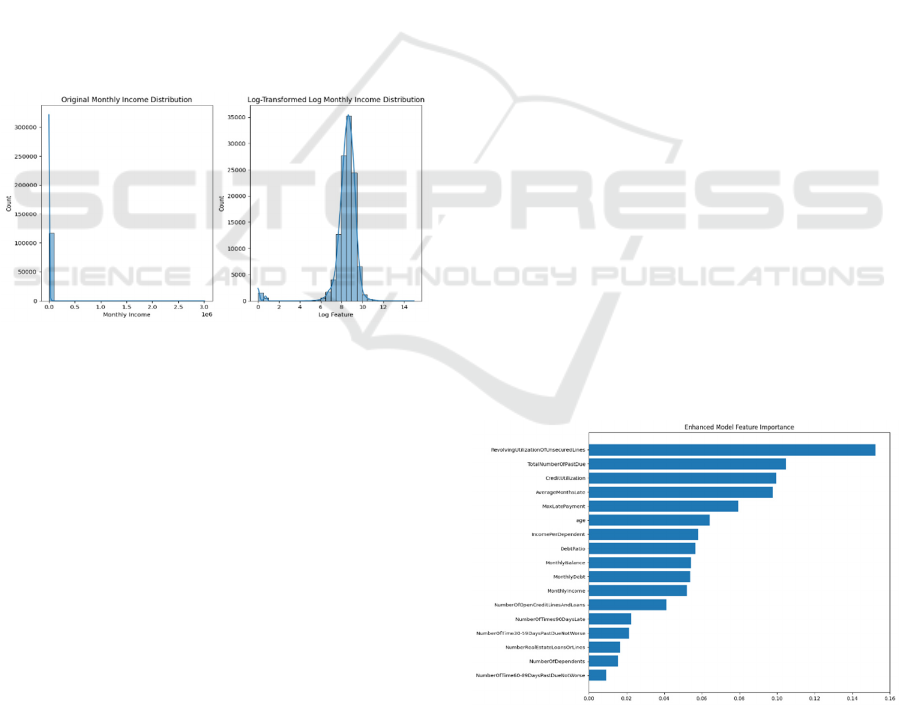

One feature engineering technique that is useful for

this dataset is the log transformation. This method is

particularly efficient for transforming features with

skewed distributions. This is because many machine

learning algorithms assume that the data is normally

distributed, therefore it may be more difficult for

some algorithms to fit such data. A good example of

a feature with skewed distribution in the GMC

dataset is the “monthly income”, as it originally

contains values that range from zero to three million.

Figure 3: Showcasing the skewed distribution of “monthly

income” before and after applying the logarithm function.

Another aspect of feature engineering is the

creation of new variables based on the observed

ones, with the role of emphasizing relationships that

otherwise would not appear in the original dataset,

resulting in an improvement in the predictive power.

The newly created features are the following:

Average Months Late;

Max Late Payment;

Monthly Debt;

Monthly Balance;

Credit Utilization;

Income Per Dependent;

Total Number of Past Due.

4.4 Class Balancing

To address the severe imbalance in the data, we

tested fifteen data-level and three algorithm-level

balancing techniques. Among the best performing

data-level methods, we mention Tomek-links (Ivan,

1976), Synthetic Minority Over-sampling Technique

(SMOTE), and Edited Nearest Neighbours (Tang et

al., 2015). Comparing the two balancing methods on

the GMC dataset, we found that algorithm-level

sampling techniques consistently outperformed

others when combined with pre-processing steps.

Most methods, like Under-sampling and Cluster

Centroids, reduced the AUC or showed minimal

improvement, with exceptions such as Tomek Links

and ENN, which performed better. However, these

improvements were still not sufficient to match the

performance achieved through algorithm-level

balancing technique.

4.5 Feature Selection

The last part of the pre-processing step was to

implement and analyse various feature selection

methods such as the Recursive Feature Elimination

(RFE) proposed by (Guyon et al., 2002), Forward &

Backward Selection, as well as the integrated

selection methods found in some machine learning

algorithms.

While the first two methods were

computationally expensive due to their iterative

nature of training and testing a model after each

modification, they produced highly comparable

results to the integrated methods. All methods

ranked the seven engineered features among the top

ten most important, even when the original features

used for their creation were ranked as the least

important, highlighting the importance of feature

engineering in producing more significant splits at

the tree level in algorithms such as the BRF.

Figure 4: Showcasing the feature importance for the model

Balanced Random Forest, highlighting the role of feature

engineering in perfecting the machine learning results.

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

252

5 EXPERIMENTS

5.1 Performance Metrics

The selection of an adequate measure for

performance is an important part of a data science

project. It offers a mathematical foundation for

comparison, assisting in the process of choosing the

most effective model and guaranteeing its

dependability in practical settings.

The most common performance measure for

classification, i.e. accuracy, can be highly

misleading in the context of imbalanced data. In the

particular case of the GMC dataset defaulters are a

small proportion of around 6% of the total

population, the trivial model predicting that all of the

samples belong to the non-defaulters class would

obtain an accuracy of around 94%. Therefore, we

decided to use the Area Under the Curve (AUC) as a

performance measure, as it is recommended also by

(Lessmann et al., 2015). Also, we have selected this

metric in order to ensure consistency with the

existing literature in the field, facilitating direct

comparisons other similar studies.

The Receiver Operating Characteristic Curve

(ROC) is drawn by calculating the True Positive

Rate (TPR) and False Positive Rate (FPR) at 𝑁

selected thresholds indexed by 𝑖. (The threshold

selection in fact controls the model's ability to

predict each class.) Let 𝑥

=FRP

and 𝑦

=TRP

be

the values of the i-th selected threshold. Then the

AUC represents the area under ROC and can be

computed by the trapezoidal rule:

AUC =

1

2

(𝑥

− 𝑥

)(𝑦

+ 𝑦

)

.

The model with greater AUC is generally

considered to be the better one.

5.2 Model Selection and Tuning

Several algorithms were tested for the task of

classifying defaulters and non-defaulters. These are:

Random Forest (RF);

Support Vector Classifier (SVC);

Logistic Regression (LR);

Extreme Gradient Boosting (XGBoost);

Balanced Random Forest (BRF);

Light Gradient Boosting Machine (LGBM);

Dense Neural Networks (DNN);

Deep Belief Networks (DBN);

TabNet.

For tuning of the models’ hyperparameters an

extensive grid search was performed for each of the

algorithms. As an example, tuning the Balanced

Random Forest model involved the testing of 19,200

combinations of parameters utilizing a 5-fold cross-

validation approach in order to identify the optimal

settings and ensure model stability.

5.3 Experimental Results

In the following we describe the experiments done

in order to improve the performance of credit

scoring models on the GMC dataset. First we have

established a baseline model which was chosen to be

the RF model tuned with grid search and 5-fold

cross-validation, without using any data pre-

processing steps such as imputation, feature

engineering or class balancing. This was set as a

reference point for further enhancements.

Then we have incorporated some data pre-

processing steps such as outlier removal and feature

engineering. This has resulted in a small

improvement of the AUC by 0.32%.

In the following step we have focused on

evaluating the effect of the different data imputation

methods (Simple Imputer, KNN Imputer and

Iterative Imputer) across five algorithms: RF

(Breiman, 2001), SVC (Hearst et al., 1998), Logistic

Regression, XGBoost (Chen et al., 2016), and

LGBM (Ke et al., 2017). The Iterative Imputer with

LGBM achieved the highest improvement in AUC

of 0.863, showing a quite significant effectiveness,

while the other imputation methods generally did not

improve performance.

Next, class balancing techniques were tested.

Cluster-based down-sampling reduced the AUC

significantly (but achieved high defaulter

classification rates), while SMOTE slightly

improved the AUC by 0.7%. In order to further

identify effective data-level balancing strategies we

have used a comprehensive grid search with several

resampling methods, for example Tomek-Links.

Algorithm-level balancing methods were compared

against data-level methods and combined

approaches. The Balanced Random Forest algorithm

outperformed all other methods, achieving the

highest AUC score and demonstrating strong

handling of class imbalance. It is based on the

original Random Forest algorithm, but during

training it ensures that all classes are equally

represented by randomly choosing a fixed number of

samples from all classes, potentially selecting the

same sample more than once. This algorithm also

has an option for employing cost-sensitive learning,

Improving Machine Learning Performance in Credit Scoring by Data Analysis and Data Pre-Processing

253

which we have tested but this did not improve in

anyway the results.

Finally, some classic neural network

architectures like the Dense Neural Networks

(DNN), Deep Belief Networks (DBN) and the new

TabNet (Arik and Pfister, 2021) were added to the

experiments. While the DNN and TabNet performed

comparably to the tree based methods with an AUC

around 0.860, DBN significantly underperformed,

highlighting its limitations for this particular dataset.

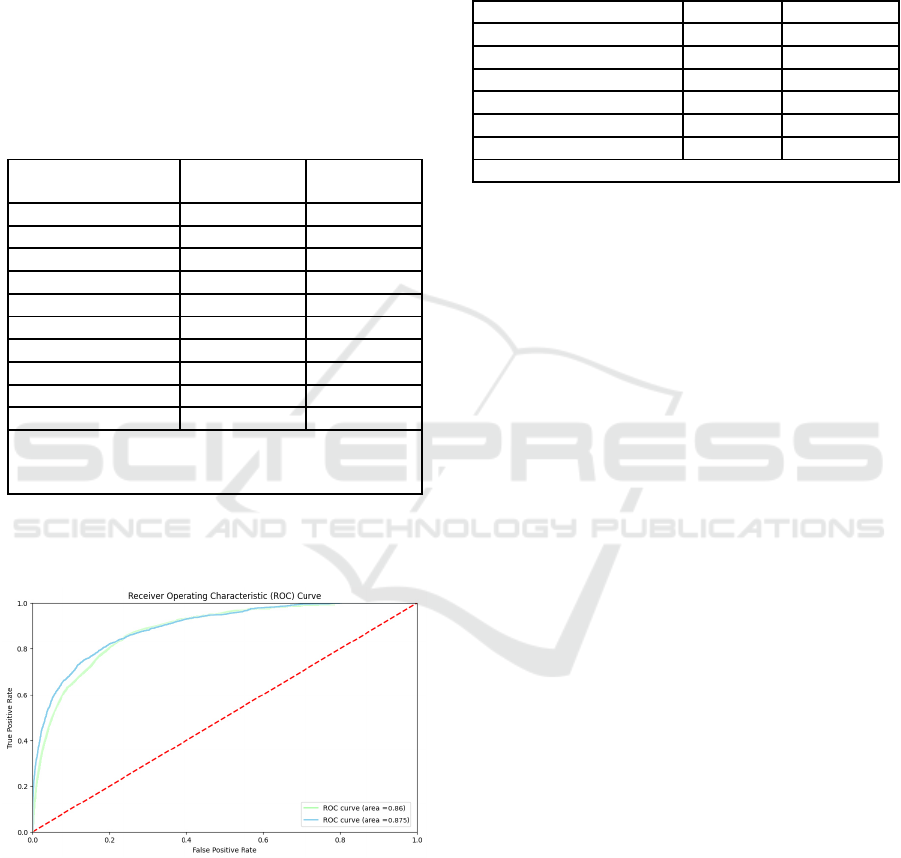

The best results obtained for each algorithm are

presented below in Table 1.

Table 1: Experimental Results.

ML algorithm

Balancing

Metho

d

AUC score

Base line RF - 0.850

RF U+TL* 0.860

SVC

- 0.770

LR - 0.804

BRF - 0.875

XGBoost

- 0.874

LGBM ENN** 0.870

DNN SMOTE 0.856

DBN - 0.773

TabNet SMOTE 0.860

Abbreviations above have the following meaning:

*

U = Under-sampling, TL = Tomek-Links

** ENN = Edited Nearest Neighbours.

The ROC of the best performing model can be

visualised and compared to TabNet in Figure 5

below.

Figure 5: ROC of the BRF model (Blue) compared to

TabNet (Green).

The final results of the experiments presented

above underscore the importance in data science of

careful data analysis, proper data pre-processing,

balancing, fine-tuning, and the selection of methods

tailored to each specific algorithm and dataset.

5.4 Comparison with Other Solutions

In Table 2 below we compare our solution to the

GMC problem with other existing solutions from the

literature.

Table 2: Comparison of our result with existing solutions.

Solution Model AUC score

(Lessmann et al., 2013) Ensemble 0.865

(

Chen, 2021

)

RF 0.797

(

Gunnarsson et al., 2021

)

XGBoost 0.848*

(

Dumitrescu et al., 2022

)

PTLR 0.857

(Gidlow, 2022) XGBoost 0.867

current BRF 0.875

* Extracted from Figure 5 in (Gunnarsson et al., 2021)

The reader should note a relative improvement

compared to the previous best existing solution by

approximatively 1% in the AUC score. Together,

these articles contributed significantly to our project

development, directed us through their previous

knowledge and discoveries, and enabled us to

achieve this new result reported here.

6 CONCLUSIONS AND FUTURE

WORK

In this paper we study how data analysis and data

pre-processing techniques can be effectively used

for credit scoring, highlighting the potential impact

of machine learning for analysing complex datasets

and enhancing decision-making in the case of

financial institutions.

The GMC dataset presents significant challenges

such as outliers, missing data and class imbalance,

necessitating robust data pre-processing in order to

improve machine learning models classification

performance. The Iterative Imputer proved to be the

most effective imputation method from those tested.

Experiments revealed that several algorithms

struggle with class imbalance, while (for this

particular dataset) the Balanced Random Forest

algorithm outperformed all of them. Through our

study we pursued a structured approach including

various stages of testing and refinement. This

emphasizes the importance of careful analysis in

developing tailored models that effectively address

data-specific challenges.

Our future work plan is to implement an

ensemble system that combines the strengths of the

BRF, XGBoost and LGBM in order to leverage the

complementary strengths of each model, enhance

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

254

predictive performance and increase robustness.

Such system may deliver superior performance as

was previously remarked in (Lessmann et al., 2013)

and (Lessmann et al., 2015).

REFERENCES

Arik, S., Pfister, T. (2021). TabNet: Attentive interpretable

tabular learning. In AAAI 2021, Proceedings of the

35th AAAI conference on artificial intelligence, pages

6679 – 6687.

Breiman, L. (2001). Random forests. Machine learning

45, pages 5 – 32.

Chen, L. (2021). Statistical Learning for Analysis of

Credit Risk Data. IOSR Journal of Mathematics 17,

pages 45 – 51.

Chen, T., Guestrin, C. (2016). XGBoost: A scalable tree

boosting system. In KDD 2016, Proceedings of the

22nd ACM International Conference on Knowledge

Discovery & Data Mining, pages 785 – 794.

Chen, C., Liaw, A., Breiman, L. (2004). Using random

forest to learn imbalanced data. University of

California Berkeley, report number 666, pages 1 – 12.

Dumitrescu, E., Hué, S., Hurlin, C., Tokpavi, S. (2022).

Machine learning for credit scoring: Improving

logistic regression with non-linear decision-tree

effects. European Journal of Operational Research

297, pages 1178 – 1192.

Gidlow, L. (2022). The Effect of Dataset Size on the

Performance of Classification Algorithms for Credit

Scoring. University of Cape Town, available at

http://hdl.handle.net/11427/37193.

Google Brain (2016). TensorFlow: A system for large-

scale machine learning. In OSDI 2016, Proceedings of

the 12th USENIX conference on Operating Systems

Design and Implementation, pages 265 – 283.

Gunnarsson, B. R., Vanden Broucke, S., Baesens, B.,

Óskarsdóttir, M., Lemahieu, W. (2021). Deep learning

for credit scoring: Do or don’t?. European Journal of

Operational Research 295, pages 292 – 305.

Guyon, I., Weston, J., Barnhill, S., Vapnik, V. (2002).

Gene selection for cancer classification using support

vector machines. Machine learning, 46, 389 – 422.

Hearst, M. A., Dumais, S. T., Osuna, E., Platt, J.,

Scholkopf, B. (1998). Support vector machines. IEEE

Intelligent Systems and their applications 13, pages 18

– 28.

Ivan, T. (1976) An Experiment with the Edited Nearest-

Neighbor Rule. IEEE Transactions on Systems, Man,

and Cybernetics 6, pages 448 – 452.

Ke, G., Meng, Q., Finley, T., Wang, T., Chen, W., Ma,

W., Ye, Q., Liu, T. Y. (2017). LightGBM: A highly

efficient gradient boosting decision tree. Advances in

neural information processing systems 30, pages 1 – 9.

Lessmann, S., Baesens, B., Seow, H. V., Thomas, L. C.

(2015). Benchmarking state-of-the-art classification

algorithms for credit scoring: An update of

research. European Journal of Operational

Research 247, pages 124 – 136.

Lessmann, S., Seow, H., Baesens, B., Thomas, L. C.

(2013). Benchmarking state-of-the-art classification

algorithms for credit scoring: A ten-year

update. Credit Research Centre, Conference Archive.

Paszke, A., Gross, S., Massa, F., Lerer, A., Bradbury, J.,

Chanan, G., Killeen, T., Lin, Z., Gimelshein, N.,

Antiga, L., Desmaison, A., Kopf, A., Yang, E.,

DeVito, Z., Raison, M., Tejani, A., Chilamkurthy, S.,

Steiner, B., Fang, L., Chintala, S. (2019). PyTorch: An

Imperative Style, High-Performance Deep Learning

Library. Advances in Neural Information Processing

Systems 32, pages 8024 – 8035.

Pedregosa, F., Varoquaux, G., Gramfort, A., Michel, V.,

Thirion, B., Grisel, O., Blondel, M., Prettenhofer, P.,

Weiss, R., Dubourg, V., Vanderplas, J., Passos, A.,

Cournapeau, D., Brucher, M., Perrot, M., &

Duchesnay, É. (2011). Scikit-learn: Machine Learning

in Python. Journal of Machine Learning Research 12,

2825 – 2830.

Tang, B., He, H. (2015). ENN: Extended nearest neighbor

method for pattern recognition. IEEE Computational

Intelligence Magazine 10, pages 52 – 60.

Improving Machine Learning Performance in Credit Scoring by Data Analysis and Data Pre-Processing

255