Building a Risk Profile for Detecting Terrorism Financing

David Makiya and Jo

˜

ao Balsa

Faculty of Sciences, University of Lisbon, Lisbon, Portugal

Keywords:

Clustering, Terrorism Financing, Risk-Profiles, Risk-Assessment.

Abstract:

This paper presents a novel and theoretical approach to detecting terrorism financing through the development

of risk-based transaction profiles using machine learning models. By integrating client and transaction data,

the proposed framework employs unsupervised clustering techniques to identify suspicious financial activities.

A multi-agent system, coupled with National Risk Indicators (NRI) and Long Short-Term Memory (LSTM)

neural networks, can enhance predictive capabilities for easier detection. The proposed model addresses the

evolving strategies of terrorist groups, offering financial institutions a dynamic and scalable tool for mitigating

terrorism financing risks while improving accuracy in anti-money laundering (AML) and counter-terrorism

financing (CTF) efforts.

1 INTRODUCTION

Terrorism is a huge threat to the socioeconomic wel-

fare of many societies. It is safe to assume that terror

activities whether state-sponsored or individual have

to be financed in one way or another. Starving the

perpetrators of such activities from access to their re-

sources forms a solid foundation towards addressing

and combating the terrorism threat. The purpose of

this work was to try to identify the pointers that can

help build a risk-based profile of active transactions

through a financial system. The aim is to cluster

transactions associated with terrorism financing into

groups associated with certain risk profiles/weights.

Challenges of establishing who a terrorist is, flag-

ging one, tracing their financial patterns, sources of

funding and other resources are important in trying

to address the issue. The infrequency and small dol-

lar amounts of some funding designs and the indi-

rect relationship between nations and operatives re-

main the biggest challenge for financial institutions to

detect this activity proactively (U.S-Treasury, 2022).

The patterns being deployed by terror groups keep

evolving with time. For example, the National Terror-

ist Financing Risk Assessment Report (US-Treasury,

2024a) from the USA identifies that ISIS financial fa-

cilitators are constantly looking for ways to consoli-

date and move funds raised in the US to shell compa-

nies around the world, thus creating layers within the

systems, thus giving a vulnerability for transactions to

circumvent monitoring by financial institutions.

The report further analyzes that ISIS supporters

may transfer funds through foreign financial institu-

tions that are not subject to the same or similar reg-

ulatory requirements as US financial institutions and

thus do not have in place effective Anti-money laun-

dering/Combating terror financing (AML/CFT) pro-

cesses or controls. Alqaeda also continues to exploit

access to the regulated financial system to support

its ongoing terrorist activities. Like ISIS, Alqaeda

has sought out non-U.S. financial institutions that

are subject to less rigorous regulatory oversight and

used them to transfer funds (US-Treasury, 2024a; US-

Treasury, 2024b).

Hizballah is not fully sanctioned by the UN and

is not classified as a terrorist organization by many

countries. For instance, while the U.S., UK, Canada,

Australia, Germany, and Israel designate Hizballah as

a terrorist group, the EU only designates its military

wing. This distinction may allow Hizballah’s political

leaders and social welfare groups to access EU bank-

ing systems (Primer, 2023). The inconsistent appli-

cation of counterterrorism sanctions by governments

and financial institutions poses challenges, as these

designations are essential for cutting off financial net-

works tied to terrorism and identifying related activi-

ties.

Research on the subject of terrorism financing has

not made it easier to distinguish it from heterogeneous

financial crimes (de Jes

´

us Rocha-Salazar et al., 2021).

In common cases, a gross categorization of money

laundering has been given the closest association to

Makiya, D. and Balsa, J.

Building a Risk Profile for Detecting Terrorism Financing.

DOI: 10.5220/0013166700003890

In Proceedings of the 17th International Conference on Agents and Artificial Intelligence (ICAART 2025) - Volume 3, pages 631-638

ISBN: 978-989-758-737-5; ISSN: 2184-433X

Copyright © 2025 by Paper published under CC license (CC BY-NC-ND 4.0)

631

terrorism financing. This study tries to build a theoret-

ical framework that can be used to quantitatively in-

form the national terrorism financing risk by innovat-

ing the NRI. The NRI can then be used as a key basis

to inform the clustering of transactions from bank sys-

tems into terror-related activities. The supplementary

objective of the work is to provide a foundation for

quantitative analysis and application based on multi-

agent systems to detect and prevent terrorism-related

activities.

2 RELATED WORKS

Since the 70s governments have tried to establish a

means of capturing and assessing money laundering

(Soltani et al., 2016). The focus on terrorism only

took direction after the September 9/11 attack in the

year 2000 at the USA (U.S-Treasury, 2022). It is

such attacks that created awareness on the need to

combat terrorism not only through the structured gun

to hand approach, but also from the financial sys-

tems of the world. The Financial Action Task Force

(FATF) unleashed some heavy regulations on the fi-

nancial systems with regards to terrorism in October

2001 (de Jes

´

us Rocha-Salazar et al., 2021). Statisti-

cal methods were used in the late 90s to detect money

laundering. Such methods mostly involved Bayesian

models and temporal sequence matching (Phua et al.,

2010). It is only after 2004 that there seems to have

been more structured focus on building systems to ac-

tively address money laundering which entailed ter-

rorism financing.

Machine-learning approaches were applied to find

money laundering patterns. (Donoho, 2004) and

(Wang and Yang, 2007) proposed decision tree algo-

rithms to detect money laundering risks. More re-

cently, (Mbiva and Correa, 2024) demonstrated the

use of unsupervised machine learning models, such

as Isolation Forest and Local Outlier Factor (LOF),

to identify suspicious transactions in migrant remit-

tances. Their model achieved a detection rate of over

90 % for terrorism financing-related transactions, fur-

ther reducing the high rate of false positives typically

seen in rule-based systems. (Tang and Yin, 2005) did

a support vector machine to detect money laundering

activities. (Liu and Zhang, 2010) proposed radial-

based function neural network model to detect money

laundering activities. A lot of effort has been put

into identifying and classifying transactions related

to Money Laundering per se. The focus of modern-

day detection systems has been rule-based classifiers.

This means that, there is an expert system, preloaded

with a certain set of pre-conditions from which, if

met, the transactions are automatically dropped into

the respective cluster that they belong to. Of course,

these methods are deficient of having a predictive ef-

fect since they are simply rule based systems (de Jes

´

us

Rocha-Salazar et al., 2021).

In trying to move away from explicit expert sys-

tems, computational models have been developed to

classify transactions as suspicious or normal (Liu and

Zhang, 2010). Computational models have been de-

veloped to classify transactions as suspicious or nor-

mal. (Labib et al., 2020) introduced social network

analysis algorithms to uncover suspicious relation-

ships between entities within transaction datasets, a

method particularly useful in identifying complex fi-

nancial networks that may be involved in terrorism

financing. This approach complements traditional

anomaly detection by focusing on the relational as-

pects of suspicious activities, offering a robust means

to detect hidden financial links The data used in Liu

and Zhang’s model of 2010 picks transaction time,

account number, transaction direction and transac-

tion amount. However, the high-dimensional nature

of financial datasets presents challenges for cluster-

ing techniques. (Bakry et al., 2024) addressed this

by applying Kernel Principal Component Analysis

(KPCA) in combination with clustering algorithms to

reduce dimensionality, improving clustering accuracy

in anti-money laundering (AML) systems. Such di-

mensionality reduction techniques are critical in han-

dling large and complex financial data while main-

taining precision in identifying suspicious patterns.

The use of a core decision tree and clustering al-

gorithms to detect money laundering was explored

with key attributes such as transaction time, sender,

receiver, frequency and transaction amount (Liu et al.,

2011). This and other mechanisms take advantage

of unsupervised learning algorithms within the do-

main. (Cao and Do, 2012) utilized the attributes

of bank transfer transactions and CLOPE algorithms

for clustering to detect money laundering in Viet-

nam. The variables used were amount sent, amount

received, number sent, number received, relationship

between what is sent and what is received and the ab-

solute value of the difference between the amounts

sent and received. In (Drezewski et al., 2015) the au-

thors analyze financial flows in order to detect money-

laundering processes. They examine the clustering of

money transfers that fulfill the specified characteris-

tics and then mine for frequent sets and sequences in

the clusters found.

In more recent works, one of the novelties of

(de Jes

´

us Rocha-Salazar et al., 2021) work was that

it compared the historical trend of each transaction

with its peer groups. As a drawback, the detection

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

632

task was entirely dependent on the nature of the trans-

action, omitting other important typologies related

to money laundering (de Jes

´

us Rocha-Salazar et al.,

2021). Some of the works directly associated with

terrorism simply try to identify the terror-related cells.

There is no direct inclination to the financial system

as there are not as many confirmed cases of terrorism

financing within financial systems. In fact, this partly

informs the need to adopt unsupervised algorithms

in the creation of risk profiles for terrorist detection

(de Jes

´

us Rocha-Salazar et al., 2021). For example,

(Koschade, 2006) tried to perform some analysis of

the communication patterns and structure of a known

terror group, the Jemaah Islamiyah cell, in order to

help predict the likely outcomes of terrorist-related

activities. Unfortunately, not much was observed

that could be directly tied to the financial systems,

aside from the probable data point that could be used

in building a non-avoidance risk-based profile. An-

other example is the prediction model CPM, designed

through a crime dataset which includes solved and un-

solved terrorist events in Istanbul between 2003 and

2005. It learnt similarities of crime incident attributes

from all terrorist attacks and then put them in appro-

priate clusters (Ozgul et al., 2009). (Gohar et al.,

2014) proposed four classification techniques to de-

tect terrorist groups, using the attributes: month, city,

country, weapon type, attack type, target and group

name. (Saidi et al., 2018) used clustering techniques

to detect cyber terrorist groups, with the attributes:

identification, date of birth, marital status, religion,

social background, position in the organization, role

in terrorist incidents, teacher and arrest dates. They

used the network data in the John Jay ARTIS Transna-

tional Terrorism Database, which identify the connec-

tions between individuals in certain attack networks

and their roles in given terrorist organizations.

2.1 How Are Risk Elements for TF

Identified?

At the National Level, most nations have adopted a

risk assessment methodology provided by the World

Bank/IMF. This is the cross-border methodology

for performing risk assessments across specific na-

tions where there is adoption of the FATF regula-

tions/guidelines (U.S-Treasury, 2022). The underly-

ing concepts for this risk assessment are threats (the

terrorists who are most active in raising/moving funds

through the financial systems), vulnerabilities (weak-

nesses that facilitate TF), consequences (the effect of

a vulnerability), and risk (the synthesis of threat, vul-

nerability, and consequence). The National Risk As-

sessment (NRA) reports within the member bodies

of ESAAMLG provide the ideal data-points from the

qualitative risk assessment going back a period of 4

years. The Risk Assessments within the member bod-

ies provide risk classifications on a scale of 0-1 on

the basis of given industries/sectors, compliance lev-

els existence of controls and etc.

Different banks apply their own methodologies to-

wards building risk profiles. So far, the tool being ap-

plied by banks are fully dependent on following the

regulators recommendations and in this context the

FATF regulations. This reduces the risk profiles to

a rule-based structure.

2.2 Relationship Between Money

Laundering and Terrorism

Financing (TF)

In building up this literature, there is clearly a lot

of work put in money laundering compared to FT.

In broad terms, money laundering and FT are both

considered financial crimes. On a higher level, we

can categorize TF as a subset of money laundering.

Therefore, most of the methodologies applicable to

combat money laundering, are also commonly used

to address TF. The only unfortunate bit is that, when

it comes to predictability, the same methods cannot be

used as the risk points are clearly different. (de Jes

´

us

Rocha-Salazar et al., 2021) makes a preclusion on the

need not to separate the two on the basis of common

typologies, techniques of execution and trends for ob-

taining or manipulating the funds. This does not re-

ally form a good basis for building accurate clusters,

particularly if we are seeking ones that can be consid-

ered pure.

The funds are moved in an almost comparative

manner. The USA Treasury has identified instances

where ISIS operatives route transactions through

complicit individuals, and in some instances shell

companies and other legal entities, to avoid detection.

Operating through shell companies is a mirror reflec-

tion with money laundering.

Money laundering is normally coupled with a

predicate offence implying that in common cases the

source of such funding would be illegal. On the con-

trary, terrorism can fully be financed by funds ob-

tained legally otherwise the criminal activity involved

would be of a non-violent nature (U.S-Treasury,

2022). For purposes of this work, it is prudent to men-

tion that this form of funding forms our focal point.

By virtue of this, we dube it ”Structured Terrorism”.

There may be some overlap in the vulnerabilities

exploited for both money laundering and TF (U.S-

Treasury, 2022). The Ministry of Finance of Re-

publica Portuguesa published a National Risk Assess-

Building a Risk Profile for Detecting Terrorism Financing

633

ment on money laundering and TF in 2015, where it

categorizes Islamist threat as a core risk point with

a high-level risk consequence (of Portugal, 2015). It

provides for factors such as, historical and political

factors, including the Judeo-Christian and ’Western’

identification, the historical connection to Al-Andalus

and Portugal’s membership of international organiza-

tions such as NATO and the EU. These are specific

aspects that will only have an impact on TF and not

money laundering. Consequently, when building a

framework for clustering, these form part of the guid-

ing pointers for risk pointers.

3 METHODOLOGY

The approach we propose through our risk analysis

profile is dependent on relying on a staging process

by adopting the multi-agent model to perform the risk

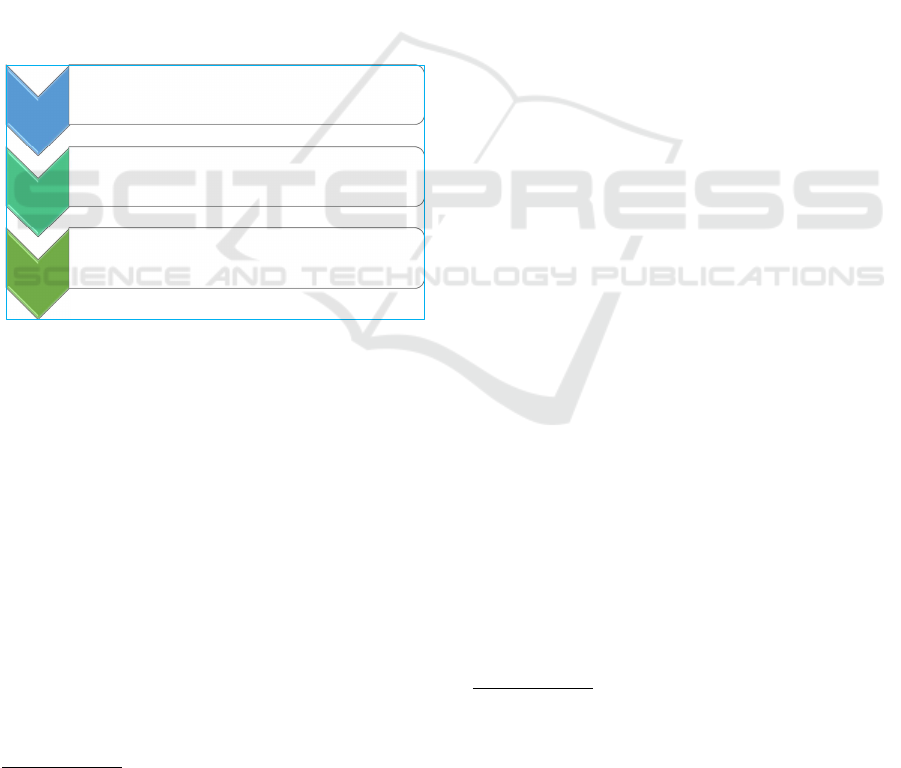

metric allocation at key stages as shown in figure 1.

Predict the

National Risk level

• Stage 1: Determine the Predictor variable through a

risk indicator that will be used to Predict the future

risk level.

Client Profiling and

Transaction

Processing

• Stage 2: Determine and allocate quantitative risk

metrics from a transaction and/or client

Risk Analysis

• Stage 3: Perform comparison of singular transaction

risk level against the defined threshold in stage 1.

Figure 1: Multi agent Adaptation General Flow Process.

Layering Risk Assessment. As per the desktop

overview, in-order to build a risk profile from the the

first stage upto the third stage, there exists 4 layers

where one is the Global Risk Level, second is the Re-

gional Risk Level, third is the National Risk Level and

lastly the bank based-risk assessment. For purposes

of this work, the focused layer is on the National Risk

Assessment and bank based-risk assessment.

3.1 National Risk Assessment

In our context, we take a quantitative methodology to

build a National Risk Profile, where instead of relying

on the qualitative National Risk Assessment reports,

we derive payments data from a national payments

system

1

and propose to co-relate with the Global Ter-

1

A national payments system is a framework of institu-

tions, policies and technologies that facilitate the transfer of

money between individuals, businesses, and governments

rorism Database™

2

based on specific risk indicators.

We provide a regression analysis methodology that

first formulates a National Risk Indicator (NRI). Sec-

ondly, we propose LSTM neural networks to predict

the future indices/values of the NRI. LSTMs are ef-

fective at handling sequential data and long-term de-

pendencies, making them suitable for detecting pat-

terns and trends in time-series data, such as terror in-

cidents and financial movements (Kader et al., 2023;

Hewamalage et al., 2021).

3.1.1 Constructing the Long Short-Term

Memory (LSTM) Neural Network

The approach for building the LSTM model ini-

tiates with an imput sequence of of the set X =

x

1

,x

2

,x

3

,...,x

t

, where x

t

represents the state of finan-

cial transactions and terror activity at time t.

f

t

= σ(W

f

· [h

t−1

,x

t

] + b

f

) (Forget Gate)

i

t

= σ(W

i

· [h

t−1

,x

t

] + b

i

) (Input Gate)

o

t

= σ(W

o

· [h

t−1

,x

t

] + b

o

) (Output Gate)

˜

C

t

= tanh(W

C

· [h

t−1

,x

t

] + b

C

)

C

t

= f

t

·C

t−1

+ i

t

·

˜

C

t

h

t

= o

t

· tanh(C

t

)

Where:

• f

t

: Forget, input and output gate activation at time

t

• C

t

: Cell state at time t

• h

t

: Hidden state at time t

• W

f

,W

i

,W

o

,W

C

: Weight matrices for forget, input,

output, and candidate cell state gates

• b

f

,b

i

,b

o

,b

C

: Bias vectors for forget, input, out-

put, and candidate cell state gates

• σ: Sigmoid activation function

• tanh: Hyperbolic tangent activation function

• x

t

: Input vector at time t

• h

t−1

: Hidden state from the previous time step

• C

t−1

: Cell state from the previous time step

LSTM will process the sequential nature of both

terror attacks and financial data to identify patterns

and relationships that can be predictive of future risks.

within a country. It includes banking networks, payment

processors and regulatory oversight.

2

The Global Terrorism Database™ (GTD) contains

over 200,000 confirmed terrorist events worldwide from

1970-2020. It includes 135+ variables on domestic and in-

ternational incidents, and is publicly available and regularly

updated.

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

634

3.1.2 Granger Causality Analysis

Secondly, to ensure that the financial variables (e.g.,

remittances, mobile payments) are useful predictors

of terror incidents, Granger Causality will be ap-

plied to assess the level of predictability of one time

series against another. This is ideal particularly since

we are working with multivariate time series struc-

tures. The novel approach proposed in (Chu et al.,

2021) enhances the detection of Granger causal struc-

tures across multivariate time series hence making it

suitable to scenarios with both single and multiple in-

dividuals or variables, thereby it is a relevant tech-

nique for time series analysis of financial and terror-

ism datasets. Since our dataset is also limited in terms

of confirmed cases, the sequential hypothesis testing

presents an adaptive method for detecting causal rela-

tionships within time series variables hence increas-

ing the chances for better performace (Devendra et al.,

2023).

In concept, for two time series X

t

(terror incidents)

and Y

t

(financial data): Under the null hypothesis, we

model time series Y

t

without the influence of X

t

:

Y

t

= α

0

+

p

∑

i=1

α

i

Y

t−i

+ ε

t

Where:

• Y

t

: Target time series at time t

• Y

t−i

: Lagged values of Y

t

• ε

t

: Error term

• p: Number of lags

On the alternative Hypothesis (Causality Exists).

The alternative hypothesis assumes that the past val-

ues of X

t

also influence Y

t

:

Y

t

= α

0

+

p

∑

i=1

α

i

Y

t−i

+

p

∑

i=1

β

i

X

t−i

+ ε

t

Where:

• X

t

: Time series suspected of causing Y

t

• β

i

: Coefficients for lagged values of X

t

The Granger causality test statistic is based on the

F-test, comparing the two models:

F =

(RSS

r

− RSS

u

)/p

RSS

u

/(n − 2p − 1)

Where:

• RSS

r

: Residual sum of squares for the restricted

model (no causality)

• RSS

u

: Residual sum of squares for the unre-

stricted model (causality exists)

• n: Number of observations

• p: Number of lags

3.1.3 Feature Engineering

To enhance predictive accuracy, features could be de-

rived based on:

• Lagging indicators: How financial transaction

volumes spike or fall days before a terror incident.

• Event proximity: Temporal closeness of a terror

event to financial anomalies.

• Volatility: Day-to-day volatility in transaction

values.

3.1.4 Model Training and NRI Calculation

The output of the LSTM model would be a score or

probability indicating the likelihood of a terror inci-

dent based on national level real-time financial trans-

actions. The training test case uses the GTD dataset

from 2001-2019 while the testing set shall adopt the

dataset from 2020-2022 to validate the model. The

National Risk Indicator (NRI) is defined to correlate

financial movements with terror incidents.

3.2 Inbank Assessment

At this level, we focus on the individualized client

profiles and transactions. We focus on manipulating

the client profiles and transactionary data to build TF

clusters by introducing the NRI.

Client Profile Data. This contains datapoints spe-

cific to the Know your Customer (KYC) and Cus-

tomer Due Diligence (CDD) requirements with re-

spect to the Financial Action Task Force (FATF

regulations). Such datapoints include the type of

client(individual/natural person), customer segment,

political exposure, economic activity, nature of the

client age of client etc.

Transactionary. This contains datapoints specific to

the occurrence of a singular transaction. They are

unique at the occurrence of each transaction like the

amount, currency, income source/purpose of funds,

geographical location, intermediary banks etc.

3.2.1 Formulating Risk Weights for Client

Profile (CP)

For CP, the primary factors involved are related to the

customer’s identity, background, and behavior. We

propose the following factors as an approach to as-

signing risk weights:

• Client Type: Are they an individual, entity, or or-

ganization? High-risk clients may include non-

profit organizations, politically exposed persons

(PEPs), or clients with a history of financial ir-

regularities.

Building a Risk Profile for Detecting Terrorism Financing

635

• Geography: Clients based in high-risk countries

(as identified by FATF) or those in conflict zones

could be assigned higher risk weights.

• Political Exposure: Politically exposed persons

(PEPs) could be flagged due to the higher risk of

being involved in corrupt or terror-related financ-

ing.

• Economic Activity: The type of business or pro-

fession the client is engaged in may be relevant.

For instance, charitable organizations or cash-

intensive businesses could be assigned higher

risks.

• Source of Funds: The origin of the funds (legal, il-

legal, suspicious) and their flow pattern over time

are critical in evaluating risk.

• Transaction History: Previous involvement in sus-

picious or unusual transactions can increase risk.

Proposed Weighting Methodology. A risk matrix

can be formulated where each factor is given a weight

based on historical data and known risk profiles. The

aggregated metric can be represented as:

RW

CP

= (Client Type)w

x

1

+ (Geography)w

x2

+

(Political Exposure)w

x

3

+ (Economic Activity)w

x

4

+

(Source of Funds)w

x

5

+ (Transaction History)w

x

6

The weights (w

x

1

,w

x

2

,w

x

3

...w

x

n

where n <= 6) can

be optimized using supervised learning techniques on

a labeled dataset where the outcome is whether the

client was linked to terrorism financing or not.

3.2.2 Formulating Risk Weights for Transaction

Profile (TP)

For TP, the focus shifts to the characteristics of spe-

cific transactions. We propose the following relevant

factors:

• Transaction Amount: Large or unusual transac-

tions, particularly in cash, could raise suspicion.

• Frequency of Transactions: Multiple small-value

transactions over a short period (structuring)

could be indicative of terrorism financing.

• Transaction Direction: The movement of funds

internationally, particularly to high-risk or sanc-

tioned jurisdictions, should raise the risk profile.

• Transaction Purpose: Whether the transaction is

for a charitable donation, cash transfer, or some

other reason. Certain purposes (e.g., donations to

regions of conflict) may increase risk.

• Intermediary Banks: Transactions routed through

offshore or lightly regulated institutions could in-

dicate risk.

• Peer Group Comparison: Comparing the transac-

tion to other transactions of similar type can help

spot anomalies.

Proposed Weighting Methodology. A similar risk

matrix for TP would consider these factors, weighted

according to their historical correlation with terrorism

financing activities. The risk score could be expressed

as:

RW

T P

= (Transaction Amount)w

j

1

+

(Frequency)w

j

2

+ (Direction)w

j

3

+ (Purpose)w

j

4

+ (Intermediary Banks)w

j

5

+ (Peer Group

Comparison)w

j

6

Again, machine learning models such as cluster-

ing algorithms could help identify the ”normal” ver-

sus ”anomalous” transactions, with outliers assigned

higher risk weights.

4 CONCEPTUAL FRAMEWORK

To integrate the risk weights for CP and TP into a

coherent detection framework, we adopt a layered

approach that builds a dynamic risk profile for each

client based on their transaction patterns and personal

information.

The combination of the methodologies for Client

Profiles (CP) and Transaction Profiles (TP) into a uni-

fied risk assessment framework can be approached

systematically by following the sequence:

4.1 Parallel Risk Scoring for CP and TP

Both CP and TP can be independently assessed to

assign risk weights based on their respective factors.

The aim here is to maintain distinct yet parallel pro-

cesses, where each profile contributes to the overall

risk score for a given entity.

• CP Risk Score (RSCP) ≡ RW

CP

: A weighted

score based on client-specific risk factors (e.g.,

geography, political exposure, client type, etc.).

• TP Risk Score (RSTP) ≡ RW

T P

: A weighted

score based on transaction-specific risk factors

(e.g., transaction amount, frequency, direction, in-

termediary banks, etc.).

This step ensures that both client- and transaction-

level risks are quantified independently but on the

same scale (e.g., 0 to 1 or 0 to 100).

4.2 Composite Risk Score (CRS)

Once the CP and TP risk scores are calculated in-

dependently, a composite risk score (CRS) can be

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

636

generated by combining them into a single metric.

The methodology to combine these two can use a

weighted or aggregated sum, represented as:

CRS = α.RW

CP

+ β.RW

T P

Where:

α and β are weights assigned to the CP and TP risk

scores respectively. These weights can be determined

based on historical analysis or expert judgment, de-

pending on which aspect (client or transaction) tends

to have a more significant impact on terrorism financ-

ing risk. If CP is more relevant (e.g., in cases in-

volving high-risk clients like politically exposed per-

sons), α might be larger than β. If TP is more relevant

(e.g. transactions involving large amounts or high-

risk countries), β would be weighted higher.

The final CRS gives a holistic view of the risk

associated with the combination of both the client’s

profile and their transactions, thus providing a com-

prehensive measure.

4.3 Dynamic Interaction Between CP

and TP

CP and TP are not isolated entities; in many cases,

the profile of the client can influence how transactions

are perceived and vice versa. Therefore, the method-

ology must account for interactions between CP and

TP, particularly for high-risk scenarios. For exam-

ple: A low-risk client may suddenly become high-risk

if there are suspicious transactions (such as unusual

amounts or transfers to high-risk countries). Or, con-

versely, a transaction flagged as high-risk could lower

in risk if it comes from a well-known, low-risk client.

To handle these dynamics, we introduce interac-

tion terms in the CRS formula:

CRS = αRW

CP

+ βRW

T P

+ γ(RW

CP

.RW

T P

)

Where:

α accounts for the interaction between CP and TP,

scaling the risk score based on how CP and TP be-

have together. For example, if both the CP and the TP

scores are high, the interaction term adds more weight

to the risk.

4.4 Thresholding and Risk Categories

The CRS can then be mapped into risk categories:

• Low Risk: CRS below a certain threshold (e.g.

CRS < 0.3).

• Medium Risk: CRS falls within a certain range

(e.g. 0.3 ≤ CRS < 0.7).

• High Risk: CRS exceeds the upper threshold (e.g.

CRS ≤ 0.7).

These thresholds can be fine-tuned based on his-

torical data, expert input, or regulatory guidelines.

Transactions or clients that fall into the high risk

category should be subjected to further scrutiny,

manual review, or automated monitoring.

As a general rule of thumb devised, when em-

ploying the aggregated NRI into the context, then a

stepped evaluation of the NRI verses the CRS can be

performed. In theory, a classifier rule that obeys the

sequence equation such that if the cumulative risk per

transaction is greater than the NRI then this qualifies

as a confirmed case of terrorism financing by virtue of

fulfilling the suspicious threshold over and above the

national risk factor. By definition, the initial work-

ing theory is that if CRS > NRI, then this implies a

confirmed case of terrorism financing.

4.5 Evaluation Metrics

To assess the performance of our proposed model,

several evaluation metrics commonly used in machine

learning can be employed, particularly for classifica-

tion and regression tasks. These metrics will help un-

derstand the effectiveness and reliability of the model

in detecting terrorism financing activities. We shall

assess the accuracy (by measure of precision and cor-

rectness ratio), sensitivity (by measure of recall and

combined with the F1-Score) and lastly true and false

positives (by assessment with a confusion matrix).

5 CONCLUSION

In this study, we proposed a framework for detect-

ing terrorism financing by building risk profiles based

on financial transactions. Our research highlights

how terrorist groups, like ISIS and Al-Qaeda, ex-

ploit regulatory inconsistencies to bypass traditional

monitoring systems. To address these challenges,

we propose unsupervised machine learning models

and multi-agent systems to cluster suspicious trans-

actions. By integrating client and transaction pro-

files with dynamic risk scoring, our approach offers a

nuanced and adaptable method for identifying terror-

ism financing. Although its effectiveness and practi-

cality need comprehensive evaluation, incorporating

the NRI and LSTM neural networks provides predic-

tive insights, significantly improving detection accu-

racy. This approach advances current AML and CTF

methodologies and offers a scalable solution for fi-

nancial institutions.

To enhance our model’s significance and prac-

ticality, we plan to address deployment challenges,

conduct broader testing across various institutions and

Building a Risk Profile for Detecting Terrorism Financing

637

regions comparatively as in (Islam and Nguyen, 2020;

Makiya and Shibwabo, 2022), and by exploring the

concept of self-sustainable multi-agent systems, eval-

uate the model’s sustainability to different financial

transactions and evolving terrorist financing methods.

REFERENCES

Bakry, A. N., Alsharkawy, A. S., Farag, M. S., and Raslan,

K. R. (2024). Combating financial crimes with unsu-

pervised learning techniques: Clustering and dimen-

sionality reduction for anti-money laundering. Al-

Azhar Bulletin of Science, 35.

Cao, D. K. and Do, P. (2012). Applying data mining in

money laundering detection for the vietnamese bank-

ing industry.

Chu, Y., Wang, X., Ma, J., Jia, K., Zhou, J., and Yang, H.

(2021). Inductive granger causal modeling for multi-

variate time series.

de Jes

´

us Rocha-Salazar, J., Segovia-Vargas, M. J., and del

Mar Camacho-Mi

˜

nano, M. (2021). Money launder-

ing and terrorism financing detection using neural net-

works and an abnormality indicator. Expert Systems

with Applications, 169.

Devendra, R., Chopra, R., and Appaiah, K. (2023). Granger

causality detection via sequential hypothesis testing.

Donoho, S. (2004). Early detection of insider trading in

option markets.

Drezewski, R., Sepielak, J., and Filipkowski, W. (2015).

The application of social network analysis algorithms

in a system supporting money laundering detection.

Information Sciences, 295:18–32.

Gohar, F., Haider, W., Qamar, U., and Butt, W. H. (2014).

Terrorist Group Prediction Using Data Classification

Data Cleansing Algorithm View project Blood glucose

monitoring and suggesting quantity of insulin for di-

abetic type one patient OR artificial pancreas (AP).

View project Terrorist Group Prediction Using Data

Classification.

Hewamalage, H., Bergmeir, C., and Bandara, K. (2021).

Recurrent neural networks for time series forecast-

ing: Current status and future directions. International

Journal of Forecasting, 37(1):388–427.

Islam, M. R. and Nguyen, N. (2020). Comparison of finan-

cial models for stock price prediction. Journal of Risk

and Financial Management, 13.

Kader, N. I. A., Yusof, U. K., Khalid, M. N. A., and Husain,

N. R. N. (2023). A review of long short-term memory

approach for time series analysis and forecasting. In

Al-Sharafi, M. A., Al-Emran, M., Al-Kabi, M. N., and

Shaalan, K., editors, Proceedings of the 2nd Interna-

tional Conference on Emerging Technologies and In-

telligent Systems, pages 12–21, Cham. Springer Inter-

national Publishing.

Koschade, S. (2006). A social network analysis of je-

maah islamiyah: The applications to counterterrorism

and intelligence. Studies in Conflict and Terrorism,

29:559–575.

Labib, N. M., Rizka, M. A., and Shokry, A. E. M. (2020).

Survey of machine learning approaches of anti-money

laundering techniques to counter terrorism finance. In

Ghalwash, A. Z., El Khameesy, N., Magdi, D. A., and

Joshi, A., editors, Internet of Things—Applications

and Future, pages 73–87, Singapore. Springer Singa-

pore.

Liu, R., Qian, X.-l., Mao, S., and Zhu, S.-z. (2011). Re-

search on anti-money laundering based on core de-

cision tree algorithm. In 2011 Chinese Control and

Decision Conference (CCDC), pages 4322–4325.

Liu, X. and Zhang, P. (2010). A scan statistics based sus-

picious transactions detection model for anti-money

laundering (aml) in financial institutions. pages 210–

213.

Makiya, D. and Shibwabo, B. (2022). A model for forex

market price prediction using deep learning. In 2022

International Conference on Innovation and Intelli-

gence for Informatics, Computing, and Technologies,

3ICT 2022, pages 195–202. Institute of Electrical and

Electronics Engineers Inc.

Mbiva, S. M. and Correa, F. M. (2024). Machine learning to

enhance the detection of terrorist financing and suspi-

cious transactions in migrant remittances. Journal of

Risk and Financial Management, 17.

of Portugal, C.-B. (2015). National risk assessment of

money laundering and terrorism assessment.

Ozgul, F., Erdem, Z., and Bowerman, C. (2009). Prediction

of unsolved terrorist attacks using group detection al-

gorithms.

Phua, C., Lee, V., Smith, K., and Gayler, R. (2010). A

comprehensive survey of data mining-based fraud de-

tection research.

Primer, T. I. (2023). U.s. sweeping sanctions on hezbollah

network.

Saidi, F., Trabelsi, Z., and Ghazela, H. B. (2018). A

novel approach for terrorist sub-communities detec-

tion based on constrained evidential clustering. vol-

ume 2018-May, pages 1–8. IEEE Computer Society.

Soltani, R., Nguyen, U. T., Yang, Y., Faghani, M., Yagoub,

A., and An, A. (2016). A new algorithm for money

laundering detection based on structural similarity. In-

stitute of Electrical and Electronics Engineers Inc.

Tang, J. and Yin, J. (2005). Developing an intelligent data

discriminating system of anti-money laundering based

on svm. pages 3453–3457.

U.S-Treasury (2022). 2022 national terrorist financing risk

assessment.

US-Treasury (2024a). 2024-national-terrorist-financing-

risk-assessment.

US-Treasury (2024b). February 2024 2024 national prolif-

eration financing risk assessment.

Wang, S.-N. and Yang, J.-G. (2007). A money laundering

risk evaluation method based on decision tree. In 2007

International Conference on Machine Learning and

Cybernetics, volume 1, pages 283–286.

ICAART 2025 - 17th International Conference on Agents and Artificial Intelligence

638